Large construction, infrastructure, energy, and industrial developments often require significant upfront capital long before they begin generating revenue. In many cases, those projects are too large, too risky, or too long-term to be funded solely through a sponsor’s balance sheet. This is where project financing becomes important.

Project financing is a method of funding a project where lenders primarily look to the project’s own cash flows, contracts, and assets for repayment, rather than relying only on the general credit strength of the project sponsors. In practical terms, it is a financing structure designed to allocate risk, secure capital, and create a framework through which a specific project can be delivered and operated.

Although project financing is often associated with banks, lenders, and financial institutions, it also has major practical implications for developers, contractors, investors, and project participants. The financing structure can influence procurement strategy, contract drafting, risk allocation, security packages, payment certainty, and the overall bankability of the project.

In this article, we explore what project financing is, how it works, and why it matters commercially for construction and infrastructure projects.

What is project financing?

Project financing is a funding structure used for large projects in which debt and equity are raised against the future revenues and contractual structure of the project itself. In simple terms, rather than lending against the sponsor’s full corporate balance sheet, lenders assess whether the project has a sufficiently reliable commercial framework to generate cash flow and repay debt.

A simpler way to think about this is as follows. If a developer wants to build a major solar farm, toll road, port terminal, or industrial plant, the lenders may not be lending because the parent company is not wealthy enough to repay the loan under any circumstance. Instead, they are lending because the project itself is expected to generate revenue, supported by contracts such as construction contracts, operating agreements, concessions (e.g. public private partnerships), and off-take arrangements (e.g. power purchase agreements/PPAs). In other words, the financing is built around the project’s ability to stand on its own commercially.

This is why project finance is closely linked to risk allocation. If the project is delayed, underperforms, fails to obtain permits, or cannot generate the forecast revenue, the financing case weakens. That is also why construction lawyers, contract managers, engineers, and developers need to understand project finance even if they are not part of the lending team.

What are the advantages of project financing?

Project financing has a number of advantages when compared with purely corporate-level funding. The main ones are:

- First, it allows very large projects to be funded without placing the full financing burden directly on the sponsor’s corporate balance sheet. That can help sponsors preserve borrowing capacity for other investments.

- Second, it allows risks to be allocated contractually among the parties best placed to manage them. For example, construction risk may sit largely with the EPC contractor, operating risk with the operator, and revenue risk partly with the off-taker or market structure.

- Third, it can make capital available for projects that might otherwise be difficult to fund through ordinary corporate lending, particularly where there is a strong contractual framework and a credible revenue model.

- Fourth, it creates a disciplined structure around approvals, reporting, testing, performance, and change control. While this can feel demanding from a delivery perspective, it can also improve transparency and reduce unmanaged risk.

By contrast, under a pure corporate-finance model, lenders are more focused on the company’s general financial strength. In project finance, lenders focus much more directly on the quality of the project itself, the reliability of its contracts, and the predictability of its cash flows.

What is the typical structure of project financing arrangements?

For a project to be financed on a project-finance basis, it will usually need to be supported by contracts, licences, approvals, technical studies, and risk-allocation arrangements that make the investment credible.

A project finance structure will commonly involve:

- project sponsors or developers

- lenders

- equity investors

- a special purpose vehicle, or SPV

- construction contractors

- operators

- off-takers or customers

- insurers

- technical, legal, and financial advisers

From a financing perspective, the key question is whether the project can stand on its own commercially. From a construction perspective, that question quickly becomes linked to programme certainty, contract structure, interface risk, permitting, cost control, and operational performance.

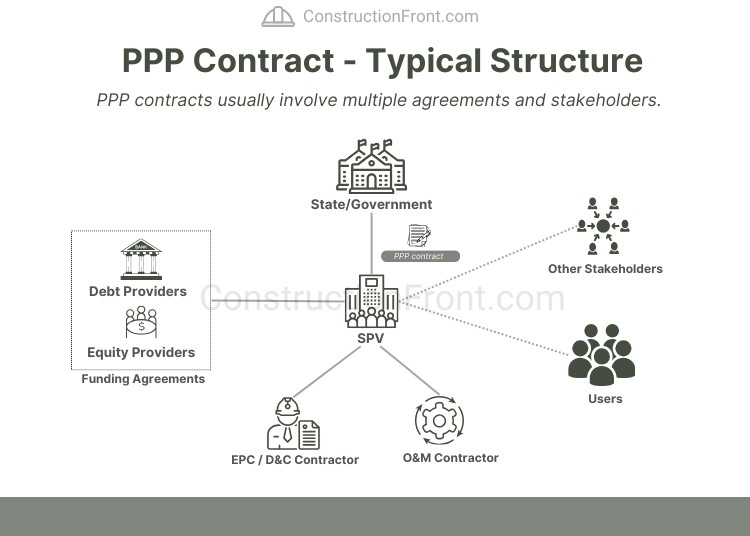

In practical terms, the SPV is central. It is the project company that signs the major project documents, borrows the money, receives project revenues, and becomes the focal point for much of the commercial and contractual structure.

For example, the structure detailed below is a common structure used in Public Private Partnership Contracts, with the SPV executing agreements with the equity and debt providers (financiers), government (as the client/owner), EPC and O&M contractors, and relationships with other stakeholders (e.g. users, other government bodies, etc).

How project financing works in practice

In a typical project finance structure, the sponsors establish a dedicated project company, often called a special purpose vehicle. That entity enters into the core contracts required to design, build, operate, and maintain the project.

Those contracts may include:

- concession or project agreements (e.g Public Private Partnerships (PPPs) agreements)

- engineering, procurement, and construction contracts

- operation and maintenance agreements

- power purchase agreements or off-take agreements

- supply agreements

- financing documents

- security documents

- insurance arrangements (e.g. performance bonds)

The lenders then assess whether the overall contractual and technical structure gives them enough confidence that the project will reach completion, operate as expected, and generate revenue.

In practice, lenders use that structure to test whether key risks are sufficiently addressed. They will usually examine whether the construction contract properly allocates delay and performance risk, whether the project has credible completion and testing mechanisms, whether there is a reliable revenue source, whether the permits and land rights are in place, and whether the project can still service debt if some assumptions deteriorate. This is why lenders often require extensive due diligence by technical, legal, insurance, and market advisers before financial close.

This is why project financing is never just about raising money. It is also about building a contract structure that supports the finance case.

Recent Examples of Project Financing

- Acciona–ACS Infra JV Reaches Financial Close on $11 Billion SR 400 Express Lanes Project

- Aecon-Pomerleau JV Reaches Financial Close on $609M Montreal Port Expansion In-Water Works

- Aypa Power Reaches Financial Close on $535 Million for California Hybrid Solar and Storage Project

- Santos secures financing for Moomba CCS Project in South Australia

Why project financing matters in construction

Project financing matters in construction because the funding structure often shapes the way the project is procured and administered. Where a project is financed on a project-finance basis, the parties usually pay much closer attention to:

- completion risk and defects

- delay risk (i.e. assessment of extension of time claims)

- cost overrun risk

- interface risk

- performance guarantees

- security packages

- insurance

- change control (i.e. variation claims and variation orders)

- lender step-in rights

- termination provisions

This affects the drafting and negotiation of construction documents. Lenders want confidence that the project will be completed on time, on budget, and to the required performance standard. As a result, construction contracts on financed projects often include more rigorous provisions around programme, testing, damages, security, and risk transfer.

In practical terms, a contractor working on a project-financed scheme may find that the finance structure sits behind many of the contract positions taken by the employer.

Typical project finance risk areas

Project financing depends heavily on risk allocation. A project may be technically viable and commercially attractive, but if the risks are not properly allocated and managed, it may still struggle to reach financial close.

| Risk area | Example |

|---|---|

| Construction risk | Delay, defects, poor coordination, cost overruns |

| Completion risk | Failure to achieve completion by the required longstop date |

| Performance risk | Plant or infrastructure does not meet output or efficiency requirements |

| Revenue risk | Demand, price, or off-take volume is lower than expected |

| Permitting risk | Delays in approvals, licences, or regulatory compliance |

| Site risk | Unexpected ground conditions (e.g. latent conditions), access issues, utility conflicts |

| Interface risk | Problems between multiple contractors, packages, or systems |

| Political or regulatory risk | Legal or policy changes affecting the project economics |

| Operational risk | Higher operating cost or lower operational performance than expected |

| Force majeure risk | External events affecting delivery or operation |

Dealing with project financing and protecting your commercial interests

Project financing is not relevant only to sponsors and lenders. It also matters to contractors, consultants, and suppliers because it affects how the project is structured and how risk is allocated.

A practical understanding of the financing framework can help project participants better understand:

- why contract terms are drafted in a certain way

- why certain approvals take longer

- why change control is tightly managed

- why completion tests are heavily negotiated

- why security and damages provisions are emphasised

- why lenders may have visibility over major project decisions

If you are a contractor

From a contractor’s perspective, a project-financed scheme usually means that completion certainty, performance, and contract discipline will be heavily scrutinised.

A contractor should therefore pay close attention to:

- completion obligations

- testing and commissioning requirements

- delay damages

- performance guarantees

- interface risks

- variation controls

- payment mechanics

- conditions tied to milestone achievement

The contractor should also understand that some employer positions may be driven not only by the employer’s own preferences, but by lender requirements sitting behind the project structure.

If you are an owner, sponsor, or developer

From a sponsor or developer perspective, project financing requires more than obtaining debt commitments. It requires building a project structure that is technically credible, contractually coherent, and commercially robust.

That usually means ensuring that:

- the project company is properly structured

- the major contracts allocate risk clearly

- the construction strategy is bankable

- the project programme is realistic

- approvals and permits are properly managed

- the lender requirements are reflected consistently across the project documents

Where these elements are weak, financing may become more expensive, more conditional, or more difficult to close.

Best practices in project financing from a construction perspective

A few practical principles are particularly important.

- Align the finance model with the project delivery strategy.

- Make sure the construction contract supports the financing assumptions.

- Avoid unrealistic programme or performance commitments.

- Manage variations and claims carefully once financing is in place.

- Keep the reporting structure disciplined and reliable.

- Understand that interface risk can undermine both delivery and bankability.

- Treat completion and commissioning obligations as core commercial issues, not just technical milestones.

Final thoughts

Project financing is more than a method of raising money. In major construction and infrastructure projects, it is a framework through which risk, contracts, cash flow, and delivery expectations are organised.

For contractors, understanding project finance helps explain why completion risk, security, testing, and change control are often negotiated so heavily. For sponsors and developers, it reinforces that bankability depends not only on the project idea, but on whether the contract structure and delivery strategy support the financing case.

Ultimately, project financing sits at the intersection of construction, contracts, and capital. That is why it matters so much to the successful delivery of major projects.

FAQs

What is project financing?

Project financing is a method of funding a project where lenders primarily rely on the project’s own contracts, assets, and future cash flow for repayment.

What is the purpose of project financing?

The purpose of project financing is to raise capital for large projects while allocating risk across the project structure, contracts, and participants.

Why is project financing important for construction contracts?

Because it influences procurement strategy, contract drafting, risk allocation, completion obligations, and the bankability of the overall project.

What is an SPV in project finance?

An SPV, or special purpose vehicle, is a dedicated project company established to own the project assets and enter into the core contracts and financing documents.

Why do lenders focus on construction contracts in project finance?

Because the project usually cannot generate revenue until it is completed and performing as required, so the construction contract is central to lender risk assessment.

Is project financing only relevant to lenders and sponsors?

No. Contractors, consultants, and suppliers are often heavily affected by project financing because it shapes risk allocation, approval processes, reporting obligations, and completion requirements.

Need Help?

Do not hesitate to contact us (click here) for specialised advice in the construction industry.

Sources

- Stefano Gatti, Project Finance in Theory and Practice: Designing, Structuring, and Financing Private and Public Projects

- E. R. Yescombe, Principles of Project Finance

- Ming Shan, Bon-Gang Hwang, and Lei Zhu, A Global Review of Sustainable Construction Project Financing: Policies, Practices, and Research Efforts

- Pranab Kumar Bhattacharya, Felix Steinbach, and Meeyoung Cho, An empirical analysis of the factors that influence infrastructure project financing by banks in select Asian economies

Disclaimer: The articles on this blog are for informational and educational purposes only and do not constitute legal or technical advice. While we strive to provide accurate and up-to-date information on construction law, regulations may vary by jurisdiction, and legal interpretations can change over time.

Newsletter

Newsletter

Stay at the front of the construction industry with the latest news, market trends, and project insights — delivered by ConstructionFront.com